For those who are leaving Japan and returning to Malaysia, one practical issue you’ll face is what to do with your Japanese brokerage account. Recently, I quit my job in Japan and returned to Malaysia for good and now I am sharing how I have dealt with my investment assets in Japan.

Most Japanese brokers require you to sell all your holdings and close your account if you were to leave the country for an extended period, as brokerage accounts are generally restricted to residents. This rule applies not only to foreigners, but also to Japanese citizens who are relocating overseas.

Each brokerage has different rules, and I will use Rakuten securities as an example here.

Table of Contents:

Why Interactive Brokers (IBKR)?

Given the weak yen, I wanted to retain my assets in Japanese yen rather than convert everything back to MYR. Unfortunately, Rakuten Trade in Malaysia is a different entity and I am not allowed to transfer my assets from Rakute Securities Japan.

After some research, as of Jan 2026, I found that Interactive Brokers (IBKR) is the only platform that allows :

- Funding in JPY

- Access to the Tokyo Stock Exchange

Below is a quick summary of the pros and cons.

Pros and Cons of IBKR

| Pros | Cons |

| Can fund directly in JPY (via Japanese banks; Wise is not supported for JPY funding) | Not directly licensed by the Securities Commission Malaysia (But regulated in US, Japan, Singapore, etc!) |

| Access to the Tokyo Stock Exchange, and more (stocks, ETFs, etc.) | Unable to fund the account in MYR |

| One global account that can be used after leaving Japan |

How:

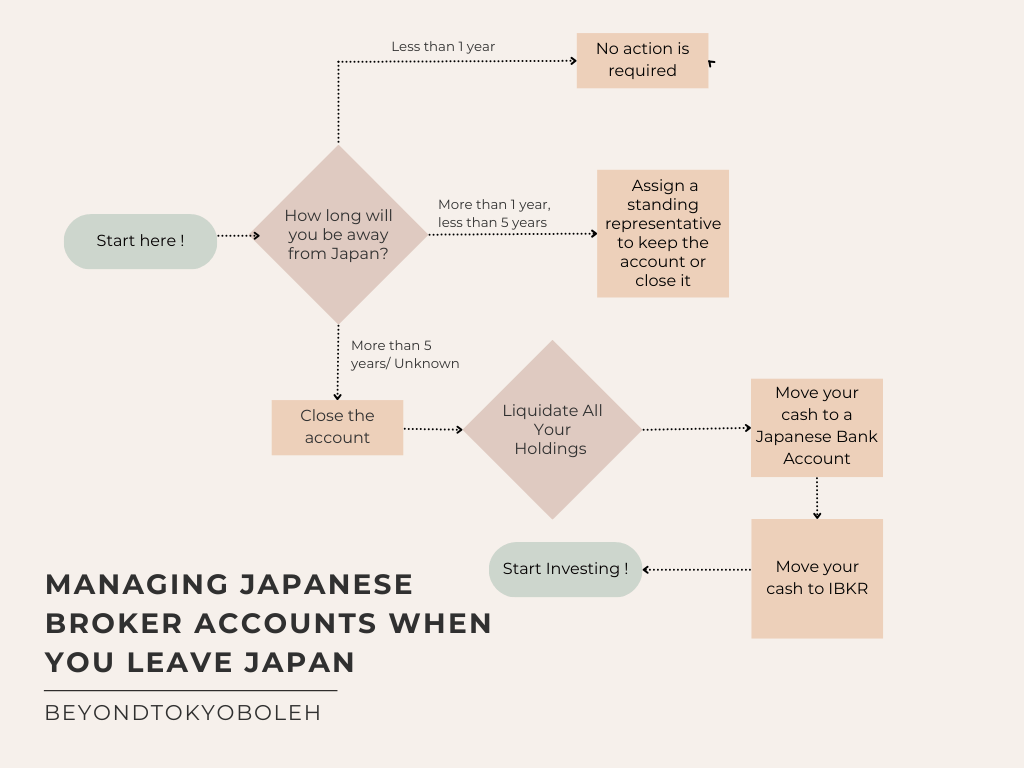

Step 1. Figure out how long you will be away from Japan

Depending on the time period, the steps to deal with your brokerage account differs.

For Rakuten Securities,

- If you are coming back to Japan within a year, No action is required

- If you will be away from Japan for more than a year and less than five years, you will need to either assign a standing representative to keep the account or close it

- Please be aware thatyou will not longer be allowed to buy but only sell securities, and terms & condition applies to the NISA account

- If you will be away from Japan for more than 5 years or time period is unclear, you are required to close it

- For more details: https://www.rakuten-sec.co.jp/web/support/procedures/non-resident/

Since I will be returning to Malaysia for more than a year and not sure if I will return, I need to liquidate all my holdings and close my brokerage account.

You can refer to this link on how to keep the account and assign a standing representative.

Step 2. Liquidate All Your Holdings

I sold all my holdings by setting limit orders to ensure that I am selling at/above a mininum price.

Step 3. Move your cash to a Japanese Bank Account

After I sold all my holdings, I moved all cash to my SMBC bank, with zero fee. The name of the bank account must be the brokerage account holder.

As mentioned earlier, Wise is not supported for JPY funding in IBKR Malaysia.

Step 4. Move your cash from Japanese Bank Account to IBKR

With SMBC bank, I can do the transfer with merely 800 yen, max 3 million yen each transaction, and max 5 million yen per month.

This can be done with overseas remittance to non residents in Yen【外国送金】非居住者円建送金

Step 5: Start Investing!

Bonus: My Investment Strategy

As of Jan 2026

I was relocating back to Malaysia and my future income will be in MYR, and I separated my investment strategy by currency.

Yen-Based Investments

- Continue investing in the Tokyo Stock Exchange (ETFs or stocks) while the yen remains weak, and hold it until the yen strengthens.

- I previously invested in an all-country index mutual fund in Japan and found a similar option:

>MUFG All Country Index ETF (Ticker: 2559) (NISA-approved)

- Low commission fees

- NISA-approved < for reference and not for tax benefits (recognized by Japan’s Ministry of Finance as suitable for long-term investment)

- Fund information:

https://maxis.am.mufg.jp/etf_fund/182559.html

I want exposure to silver without the hassle of physical storage:

>MUFG Silver-Backed ETF (NISA-approved)

- No equivalent silver-backed ETF is available in Malaysia as of January 2026

- More information:

https://kikinzoku.tr.mufg.jp/en/lineup/silver.html

MYR-Based Investments (Salary in Malaysia)

For income earned in MYR:

- Cash deposits (for emergency funds)

- Gold (physical gold or e-Gold backed by 999.9 fine gold)

- Stock markets (US, Singapore, etc.)

With IBKR, You can only invest overseas by converting MYR into foreign currencies in funding your account. Wise has one of the best rates.

Useful guide:

https://ringgitfreedom.com/investing/beginners-guide-investing-abroad-via-interactive-brokers-from-malaysia/#h-is-interactive-brokers-approved-by-securities-commission-malaysia

Final Thoughts

Relocating countries doesn’t mean I have to give up everything and start from zero. With the right broker and a clear currency-based strategy, I have retained my yen exposure, stay invested in Japan, and smoothly transition my assets back to Malaysia when the yen rate is not favourable.

I hope this article helps those who are relocating — or planning to relocate their assets — to Malaysia and are thinking about how best to manage their Japanese investments.

*In Malaysia ,capital gains and dividends are generally tax-exempt (withholding taxes might be applicable), which makes investing attractive.

Disclaimer: This site provides information only. Nothing on the site should be construed as investment advice. You must do your own research and make your own decisions. If in doubt, please consult a professional accountant or independent financial advisor.

Leave a comment