Read time ⏲

When you walk up to a bank counter in Malaysia to run some simple errands, at times, the banker will start promoting their mutual funds. They will usually ask about your risk tolerance, investment experience, etc. However, what they often do not explain is how those funds are structured—whether they are active or passive, and more importantly, how much you are paying in fees. Bankers will distract you by focusing on the gross return and not the net return!

Before investing in any funds, a basic rule of thumb is to understand the difference between active and passive funds.

Why is it so important and why is not the banker explaining to you in the first place?

The short answer: fees

Fund fees have a direct impact on your long-term returns — and on the banks’ profitability.

In this article, we will talk about what passive funds are, how they differ from active funds, and where to find them in Malaysia.

Table of Content

What are Passive funds?

In short, the investment strategy of a passive fund is to mimic the performance of a basket of companies, such as the S&P 500 index, by investing in the same companies that make up the index.

In practice, much of this process can be automated. Besides, unlike active funds, passive funds do not involve stock picking, thus no need a team of equity researchers to analyze companies’ stock.

Without equity research and portfolio manager making frequent buy-and-sell decisions, operating cost are significantly lower. As a result, this leads to LOWER FEES for investors!

Low Operating Cost = Low Fees for Investors

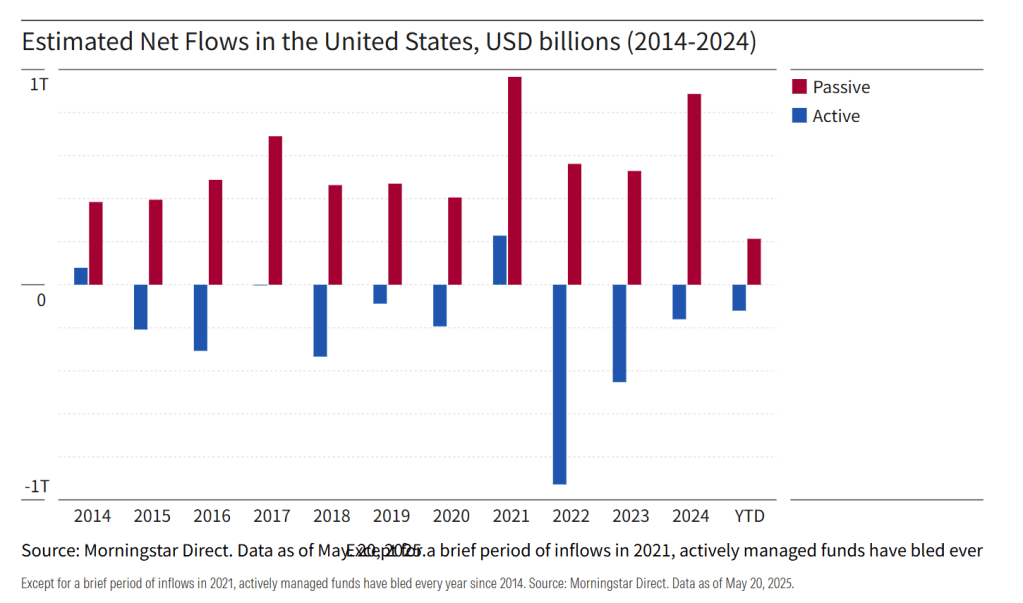

In the past 10 years, people were buying more passive funds than active funds in the U.S, highlighting their growing popularity worldwide.

Active vs Passive

Key Differences

| Active Funds | Passive Funds |

|---|---|

| Aim to beat the market, such as S&P 500 | Aim to mirror the performance of an index |

| ✓ Stock picking + equity research | Selection of stock is rules-based, and generally automated ✖ equity research |

| Believes that the market is inefficient, thus the opportunity to make money | Believes the market is efficient and beating market is highly unlikely |

| Higher turnover →potential higher capital gain tax | Long term holding→low capital gain tax |

| High operating cost + Performance fee | Low operating cost |

Can Active Managers really beat the market? or is it merely marketing?

It might be true that some active managers are well experienced and very dedicated, hence able to produce a higher return than the index, such as S&P 500, however, on an after-tax basis, this might not be the case.

Some argue that active managers underperform because the benchmark index is not an appropriate comparison due to different investment strategies.

But let’s be honest — how many individual investors actually care about benchmark technicalities? — they care about results.

If a fund consistently delivers lower returns than alternatives, then the investor is simply not getting the best use of their money.

Don’t forget the power of compounding!

Compounding interest means you earn from both the initial money you put in + the interest you earn.

As more interest you earn, more will be added to the initial money, making your money grow faster.

A simple way to understand compound interest is to think of it like a contagious virus, such as the coronavirus.

if one person get infected, that person might transmit the virus to another person. Now we have 2 people who are contagious, which then might infect 4, then 8, and so on, accerlerating the growth rate of people getting infected.

Compound interest works the same way.

Your returns generate more returns, creating a snowball effect over time.

A small difference in net return might not seem like a huge deal in the short term, however in the long term, the divergence could be significant.

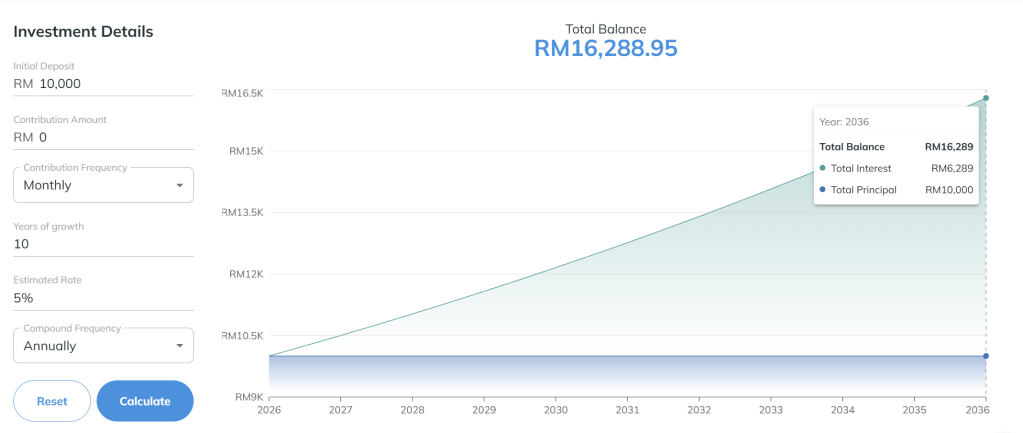

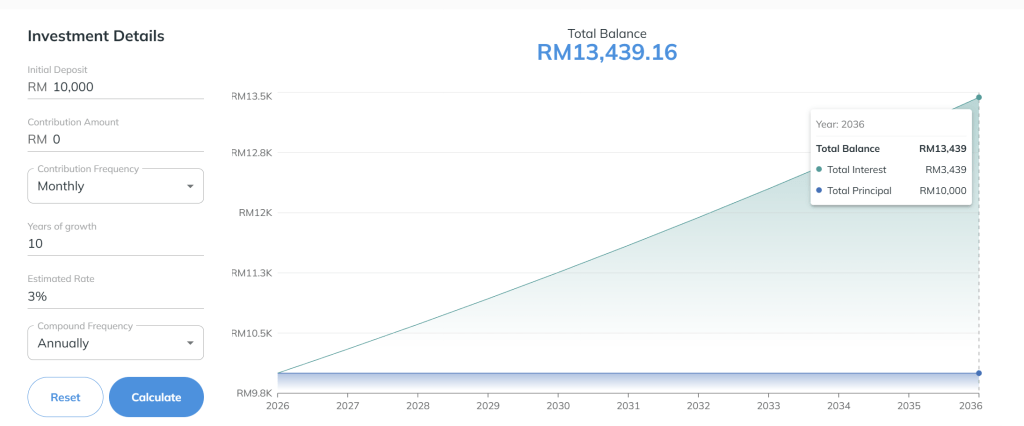

Let’s assume that we invested RM10,000 in 2 funds that generate 5% and 3% net return on average in a 10-year period respectively.

By using the calculator, we know that this leads to a total of RM2,849.79 difference!

Net Return: 5%

In 10 years,

- Total balance: RM10,000→ RM16,288.95

- Total Interest → RM6,288.95

- Overall Return→ 62%

Net Return: 3%

In 10 years,

- Total balance: RM10,000→ RM13,439.16

- Total Interest → RM3,439.16

- Overall Return → 34%

Passive funds in Malaysia

As of 2026, truly low-cost passive funds in Malaysia are still limited.

Why so? The possibile reasons are as follow:

- Thin profit margin for asset management firms

- Lack of advanced automation and technology, leading to higher costs

- human intervention is needed,which pushes fees up.

- No strict regulation enforcing fiduciary duty, meaning firms are not always required to put clients’ interest first

- Lack of demand

Don’t Give Up Hope Yet!

Thanks to online brokerage, we can now access overseas market easily from our phones.

Rakuten trade, IBKR, etc, offer access to U.S., HK, Singapore market, where low cost passive ETFs are widely available.

The main trade-off is that we need to convert MYR to foreign currencies, which leads to forex risk.

Hopefully, in the future, there will be more low cost passive funds denominated in MYR, — similar to Japan (such as MUFG’s 0.06% passive mutual funds in Japan) and in the U.S., (such as VOO that offers expense ratio 0.03% index funds).

Disclaimer: This site provides information only. Nothing on the site should be construed as investment advice. You must do your own research and make your own decisions. If in doubt, please consult a professional accountant or independent financial advisor.

Leave a comment