Read time

Back In Japan,whenever I talked to my Japanese friends about the stock market, their reaction was usually:

“I’m not sure… it’s too complicated for me.”

The conversation would quickly end.

But in Malaysia, once I started the conversation, the opposite happens —

everyone suddenly has something to say.

People start sharing opinions, strategies, hot stocks, property prices, ETFs, crypto… and the discussion never stops.

This contrast surprised me.

In this article, I will talk about my personal observations on the investing culture differences between Japan and Malaysia.

Table of Contents

- Table of Contents

- 1. The First Impression: Conversations About Money

- 2. Perception towards Money; Savings vs Investing Mindset

- Conclusion

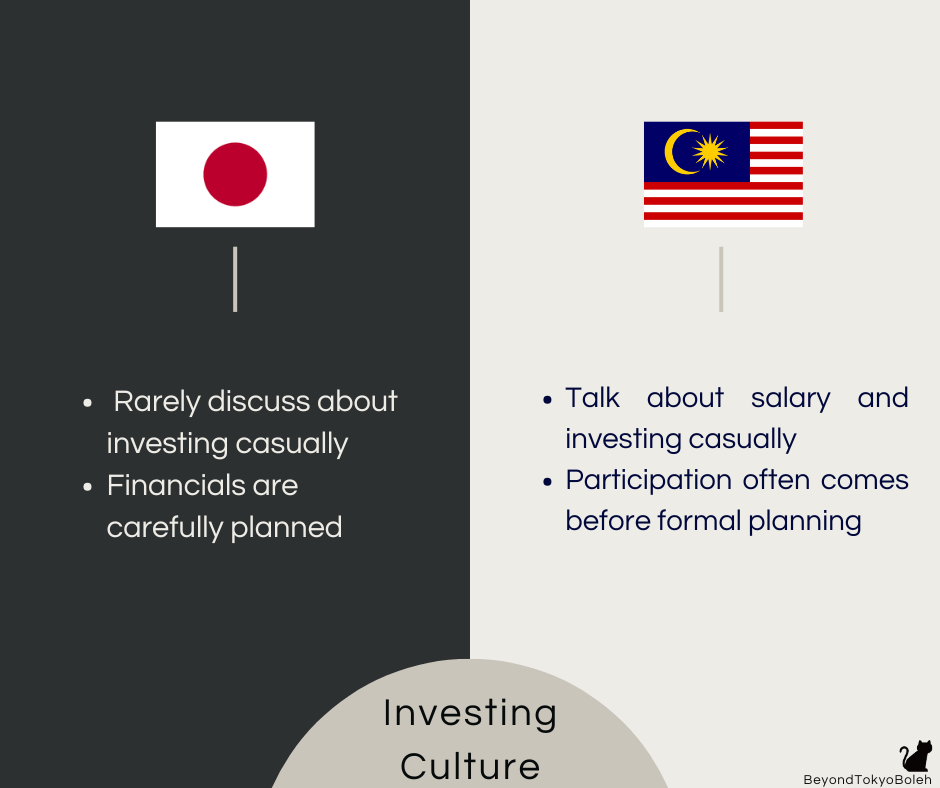

1. The First Impression: Conversations About Money

Japan

- Even among friends, we rarely discuss about investing casually (just like politics, everybody has different opnions, and Japanese tend to avoid discussions that may create conflicts)

- Financials are carefully planned (having a household account book is common)

Malaysia

- Talk about salary and investing casually. Market movements quickly become social topics

- Participation often comes before formal planning

2. Perception towards Money; Savings vs Investing Mindset

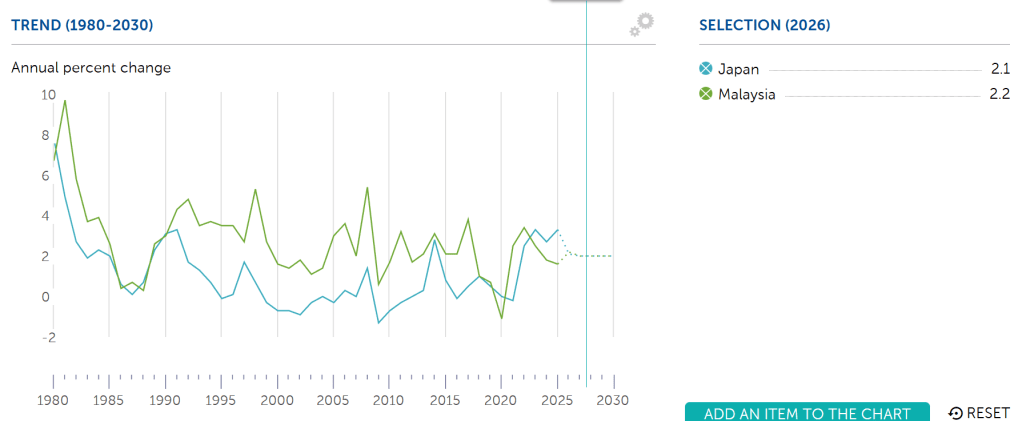

To understand the behaviour, we need to look at economic background.

Source: https://www.imf.org/external/datamapper/PCPIPCH@WEO/JPN/MYS

Background:

Japan experienced long periods of deflation until recently.

While economists often say deflation is bad for the country, as a consumer, it is one of the best things as I do not have to worry about prices going up + savings maintain their purchasing power.

Malaysia, on the other hand, has consistently experienced inflation.

Prices rise every year.

Cash loses value. So people naturally look for ways to protect their wealth via investing.

Click the arrow to view more

Japan: Stability and Deflation

Undeniably, Japan has one of the top 10 highest GDP in the world, and has many local big firms with global footprint.

Locals can become well off by climbing up the corporate ladder + deflation (prices were stable for years), hence, there wasn’t much need to invest.

Besides that, Japanese people are one of the most hardworking people in the world. Many believe money should be earned actively, and passive income is dirty. With that perception, some people avoid investing.

Moreoever, with the stock market crash during 1990 bubble, people has lost trust in the stock market.

However, this is changing:

With an aging population and inflation, government started a program called NISA to help its citizens combat inflation. NISA is a tax free investment account where citizens are not taxed when investing in stocks or approved funds.

The government has also been working with the financial institution to improve financial literacy and encouraging people to invest long term, diversify their portfolio and start small.

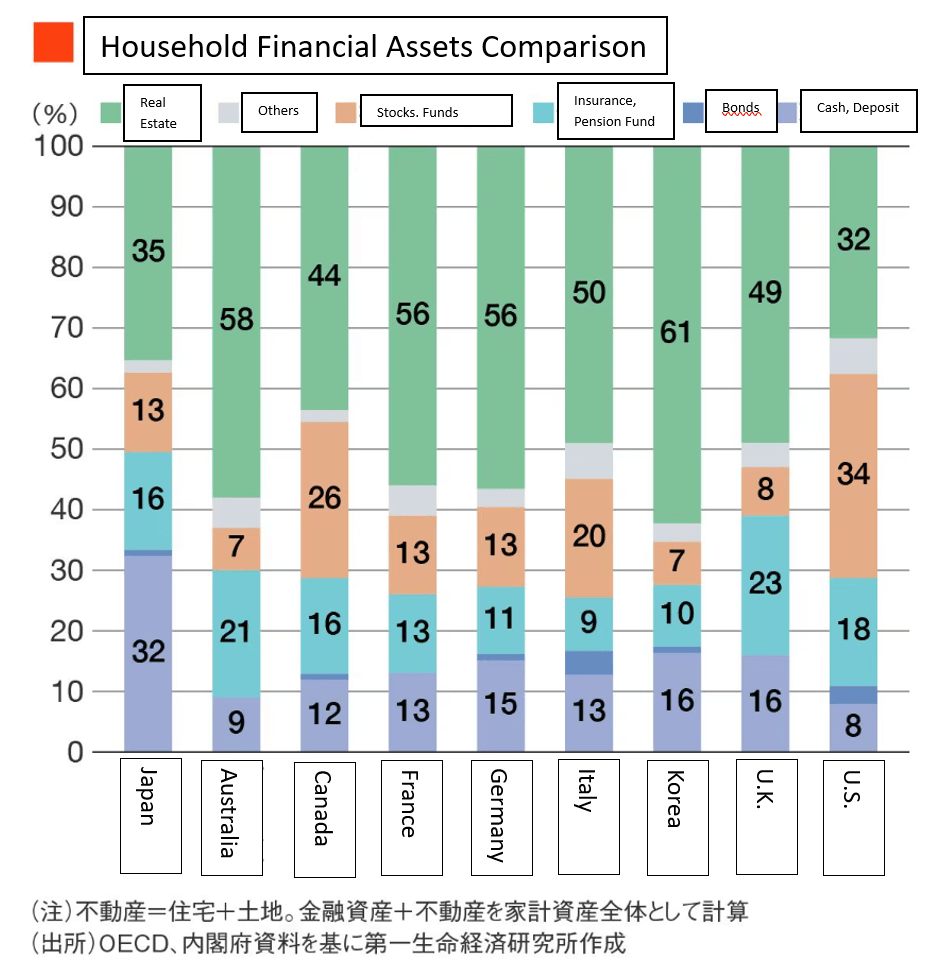

As a result, Althought Japan’s saving rate is still the highest among OECD countries, participation in investment markets has been steadily increasing, with investment ratio equivalent to France and Germany, and higher than Korea and the UK.

Malaysia: Inflation and Urgency

In Malaysia, the situation is reversed.

Inflation makes cash lose value over time.

Doing nothing feels like moving backwards.

So people start asking:

- How do I grow my money?

- How do I beat inflation?

- Where should I allocate my savings?

Moreover, Malaysia has higher geopolitical risk, so people tend to invest overseas to hedge the Malaysia ringgit.

Conclusion

Neither is better than the other.

Japan shows the importance of education, planning, and discipline before taking risk.

Malaysia shows the importance of initiative and protecting purchasing power instead of relying purely on savings and the government.

The most resilient mindset probably combines both:

Japanese caution with Malaysian adaptability.

And perhaps most importantly, attitudes toward money conversations differ across cultures, so it helps to understand people’s comfort levels before starting the conversation.

Leave a comment