Read time ⏲

Now that you know what your net worth is, and how much money you want to have in the future…

The next step is simple:

- Track how much you are making

- Track how much you spend

- how much you are saving

If we don’t track our money, we won’t know where it goes.

And if we don’t save, we can’t invest.

And if we don’t invest, our money won’t grow.

In this article, we will talk about how to track your money and create your own financial statements.

Table of Contents

Why Should We Do This?

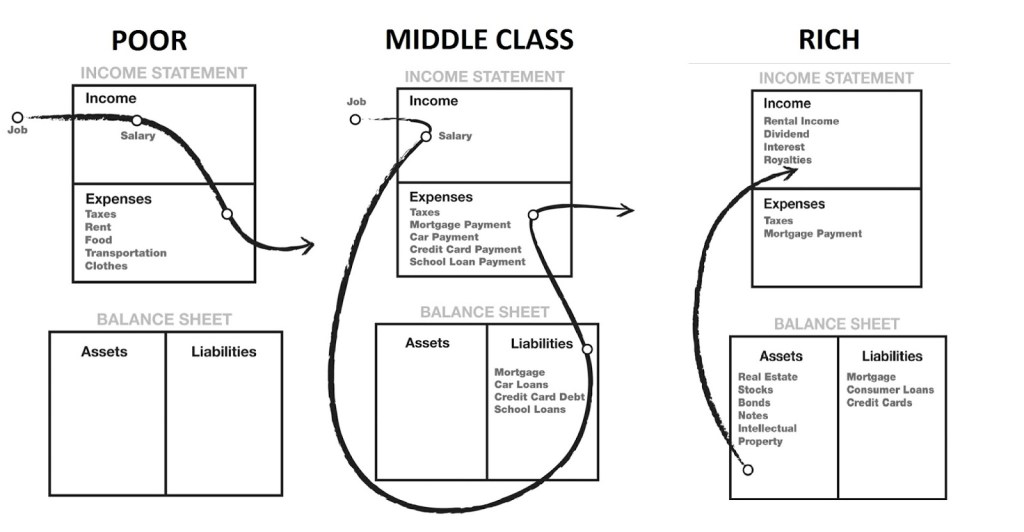

Back in school, I learned how to create balance sheets, income statements and how to do journals for companies.

One day, I came across this book, “Rich dad, poor dad” by Robert Kiyosaki, and I realized, “Damn, I can use this accounting knowledge for my own financial planning. I can create my own balance sheets and income statements.”

According to the book “Rich dad, poor dad”:

- The Poor: spend everything they earn, and has 0 savings

- The Middle Class: use their salary to repay their debts and spend the rest, and has 0 savings

- The Rich: buy assets that generate income

Not everyone aims to be rich, but to get from point A to point B, we need our money to work for us.

Reason: We only have 24 hours a day, we cannot work forever.

How to create one?

It’s very simple. Just 2 steps.

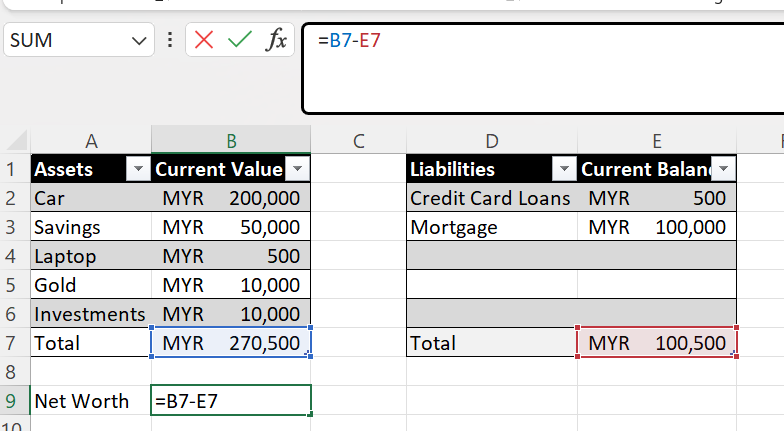

On previous post, we calculated our net worth, as well as created our own balance sheet.

Now, lets create our income statements.

1. Track how much you are earning and spending each month

Write down:

- How much money you earn

- How much money you spend

- What you spend it on

You can:

- Use any budgeting app

- Use a notebook

- Use your bank or credit card statement

It is important to record the category of spending to identify any redundant expenses.

For example:

You do not have extra money left this month and by looking at the expenses’ details, you realized you have bought too many lattes.

Personally, I record it on my Japanese app whenever I spend. I did not link it to my bank accounts due to security issue as well as I want to be concious of my spending each time.

The drawback?

I can get paranoid sometimes if I had a big spending in the beginning of the month.

The upside?

Its all worth it when I see that I am spending within budget by the end of the month.

For income, I download my payslip as well as broker statement manually.

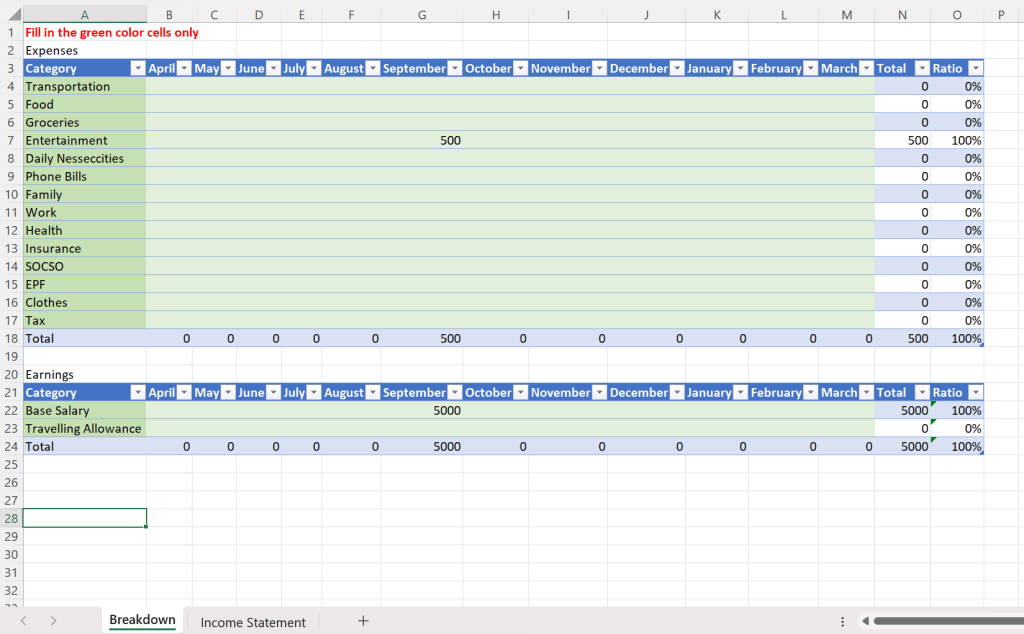

2. Put Everything Into Excel

At the end of the month, input your income and expenses into an Excel spreadsheet.

I have already created the template for you so that you can dive right in!

Subscribe below to get it!

In the “Breakdown” tab:

- Fill in the green cells

- Customize categories based on your lifestyle

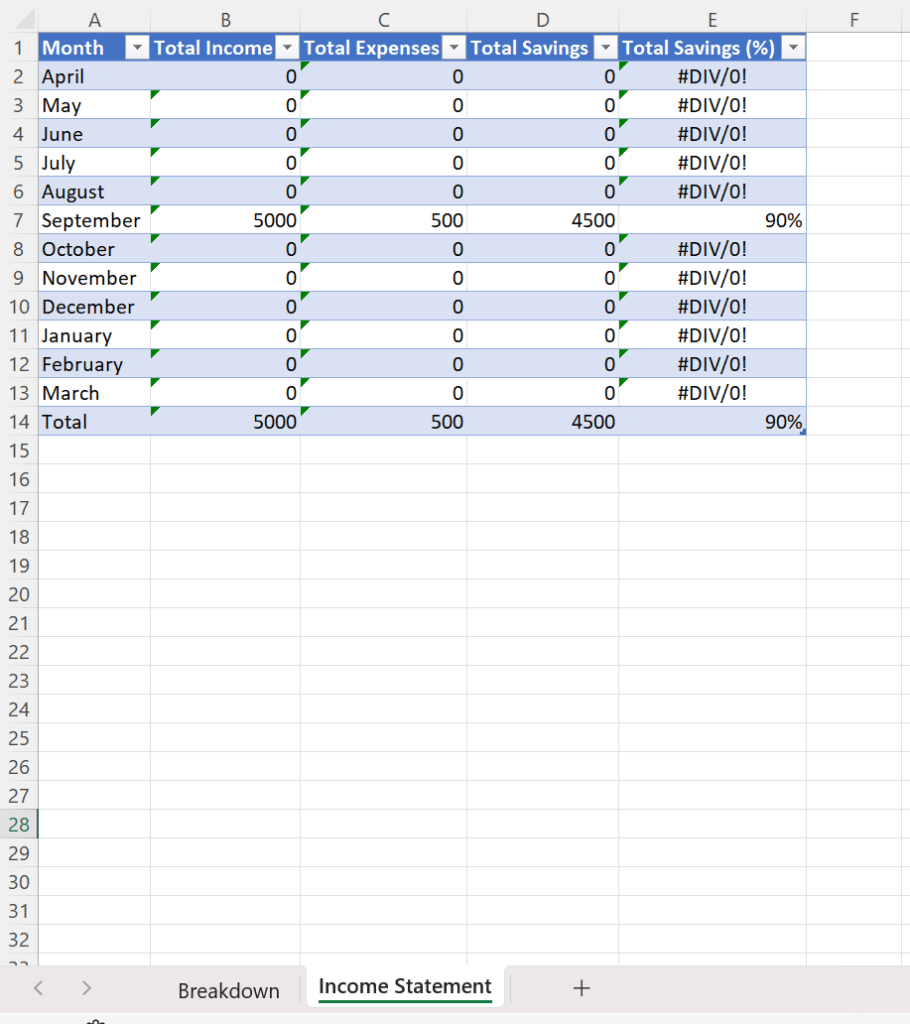

Your income statement will be automatically created on the next tab.

Now let’s think like a CFO of your own life!

Analyse how much you have left for investment

On the ” Income Statement” tab, analyse how much you have left.

Money Left= Savings = Money you can invest

Total Savings is the amount that you are putting in the assets column on your balance sheet.

A rule of thumb is to save 20% of your income, however, if you want to be more aggressive, saving rate of 50% or above is recommended.

But be realistic.

Don’t set a target that is too hard!

Questions to ask:

- Did I reach my target saving rate?

- If not, what did I overspend on?

- Can I reduce/ eliminate certain expenses next month?

- Is the target saving rate realistic?

Reflection and Improving just a little every month is very powerful, just like the Japanese Business Philosophy, “Kaizen”, which focuses on continuous small improvements.

Conclusion

Creating personal financial statements isn’t about restriction.

It’s about clarity.

When you track your money:

- You stop guessing.

- You stop feeling guilty.

- You start making decisions based on facts.

You visualize your money flow based on data.

Over time, as you have more control of your money,

you have more control of your life.

Now that we know where our money goes each month, we can now plan how to reach our target net worth.

Leave a comment